With Congress back in their districts for August Recess, we thought it’d be a good time to talk about a some federal issues that are a high priority for Farm Bureau. First up this week: tax reform.

Congress is starting to get serious about tax reform. Both the President and leaders in Congress say they want to develop a tax reform plan this fall. But what will it look like? Will it include the things farmers need to be successful?

Agriculture operates in a world of uncertainty. From unpredictable commodity and product markets to fluctuating input prices, from uncertain weather to insect or disease outbreaks, running a farm business is challenging under the best of circumstances. Farmers need a tax code that recognizes their unique financial challenges.

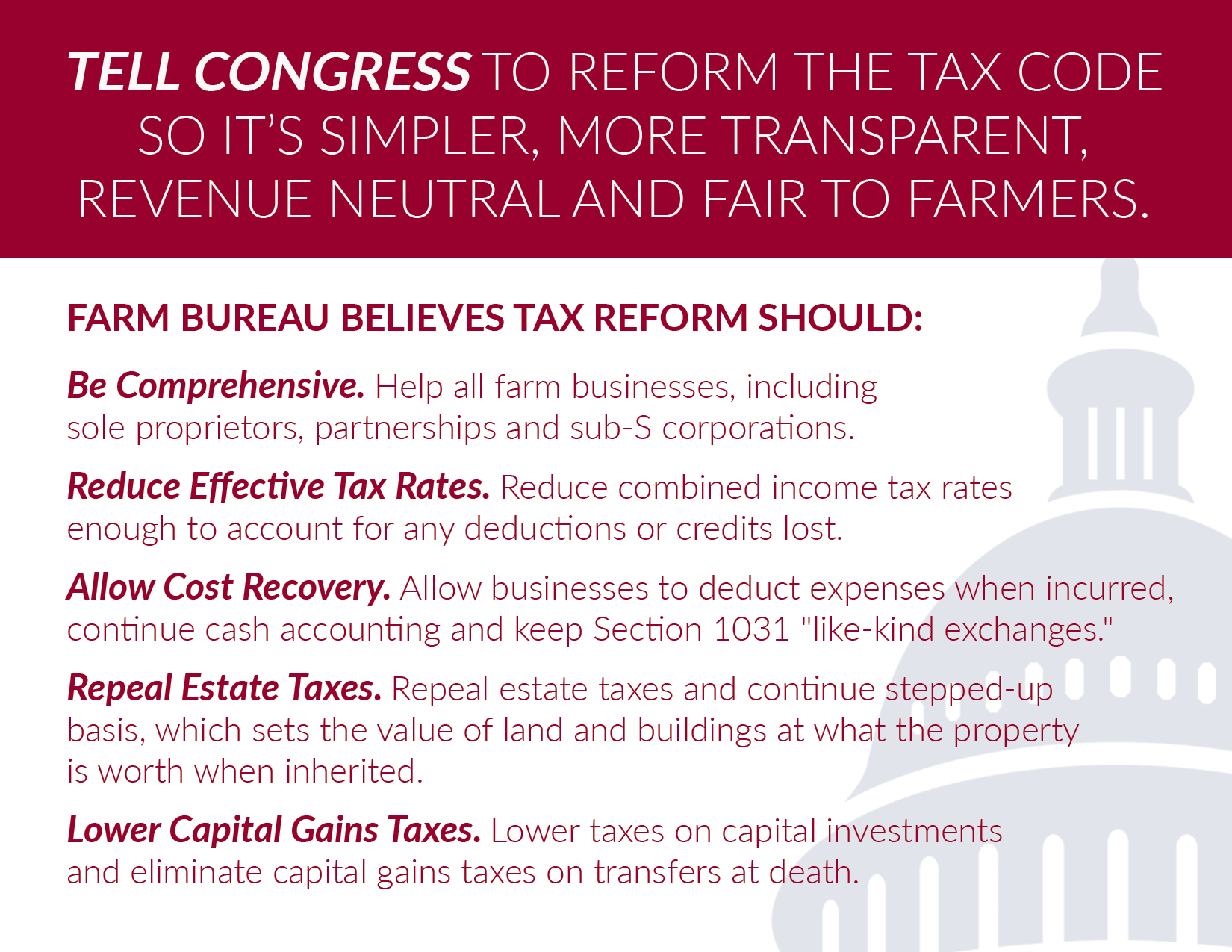

Farm Bureau supports replacing the current federal income tax with a fair and equitable tax system that encourages success, savings, investment and entrepreneurship. We believe that the new code should be simple, transparent, revenue-neutral and fair to farmers.

Farm Bureau believes tax reform should:

- Be Comprehensive: Help all farm businesses, including sole proprietors, partnerships and sub-S corporations.

Any tax reform proposal considered by Congress must be comprehensive and include individual as well as corporate tax reform. More than 96 percent of farms and 75 percent of farm sales are taxed under IRS provisions affecting individual taxpayers. Any tax reform proposal that fails to include the individual tax code will not help, and could even hurt, the bulk of agricultural producers who operate outside of the corporate tax code.

- Reduce Effective Tax Rates: Reduce combined income tax rates enough to account for any deductions or credits lost.

Any tax reform plan that lowers rates by expanding the base should not increase the tax burden of farm businesses. Because profit margins in farming are tight, farm businesses are more likely to fall into lower tax brackets. Tax reform plans that fail to factor in the impact of lost deductions for all rate brackets could result in a tax increase for agriculture.

- Allow Cost Recovery: Allow businesses to deduct expenses when incurred, continue cash accounting and keep Section 1031 “like-kind exchanges.”

Cash accounting is the preferred method of accounting for farmers because it provides the flexibility needed to optimize cash flow for business success, plan for business purchases and manage taxes.

Because production agriculture has high input costs, farmers place a high value on immediate expensing of equipment, production supplies and preproductive costs. This includes fertilizer and soil conditioners, soil and water conservation expenditures, the cost of raising dairy and breeding cattle, the cost of raising timber, endangered species recovery expenditures and reforestation expenses. Farm Bureau also places a priority on Sect. 179 small business expensing and supports bonus depreciation, shorted depreciation schedules, and the carry forward and back of unused deductions and credits.

- Repeal Estate Taxes: Repeal estate taxes and continue stepped-up basis, which sets the value of land and buildings at what the property is worth when inherited.

Farm Bureau supports permanent repeal of federal estate taxes. Until permanent repeal is achieved, the exemption should be increased, indexed for inflation and continue to provide for portability between spouses. Full unlimited stepped-up basis at death must be included in any estate tax reform. Farmland owners should have the option of unlimited current use valuation for estate tax purposes.

- Lower Capital Gains Taxes: Lower taxes on capital investments and eliminate capital gains taxes on transfers at death.

Farm Bureau supports eliminating the capital gains tax. Until this is possible, the tax rate should be reduced and assets should be indexed for inflation. In addition, there should be an exclusion for agricultural land that remains in production, for transfers of farm business assets between family members, for farmland preservation easements and development rights, and for land taken by eminent domain. Taxes should be deferred when the proceeds are deposited into a retirement account. Farm Bureau supports the continuation of stepped-up basis.

We need to ensure that North Carolina’s US Representatives and Senators are engaged in the tax reform process and that they fully understand the needs of farmers. If you are a farmer or are involved in agriculture, we need you to contact your representatives and tell them why tax reform is import to your farm. And while they are back in the district, have conversations with them about tax reform at meetings, town halls, fairs and local events.